This piece was picked up by The Press and STUFF last week, which was nice.

Regular readers might recognise it as a rework of a previous post where I was making a case that arguments over public asset sales distracted from an easier debate over asset allocation. Since I didn’t get any bites about this orginal piece I was in the process of reworking it, pointing out that asset sales were happening under a different guise, when the whole topic hit the papers again. So in it went.

I think the big lesson here is that if I want to get published in the paper regularly I will probably need 3-5 topics on the slow burn so I can take advantage of what is topical. I am not sure if I have that many topics! 🙂

The other interesting thing is that although it was in the paper (great!) to get rapid feedback you need to be on the front section of STUFF. In all there were only 12 comments, which was a bit of a fail really.

_____________________________

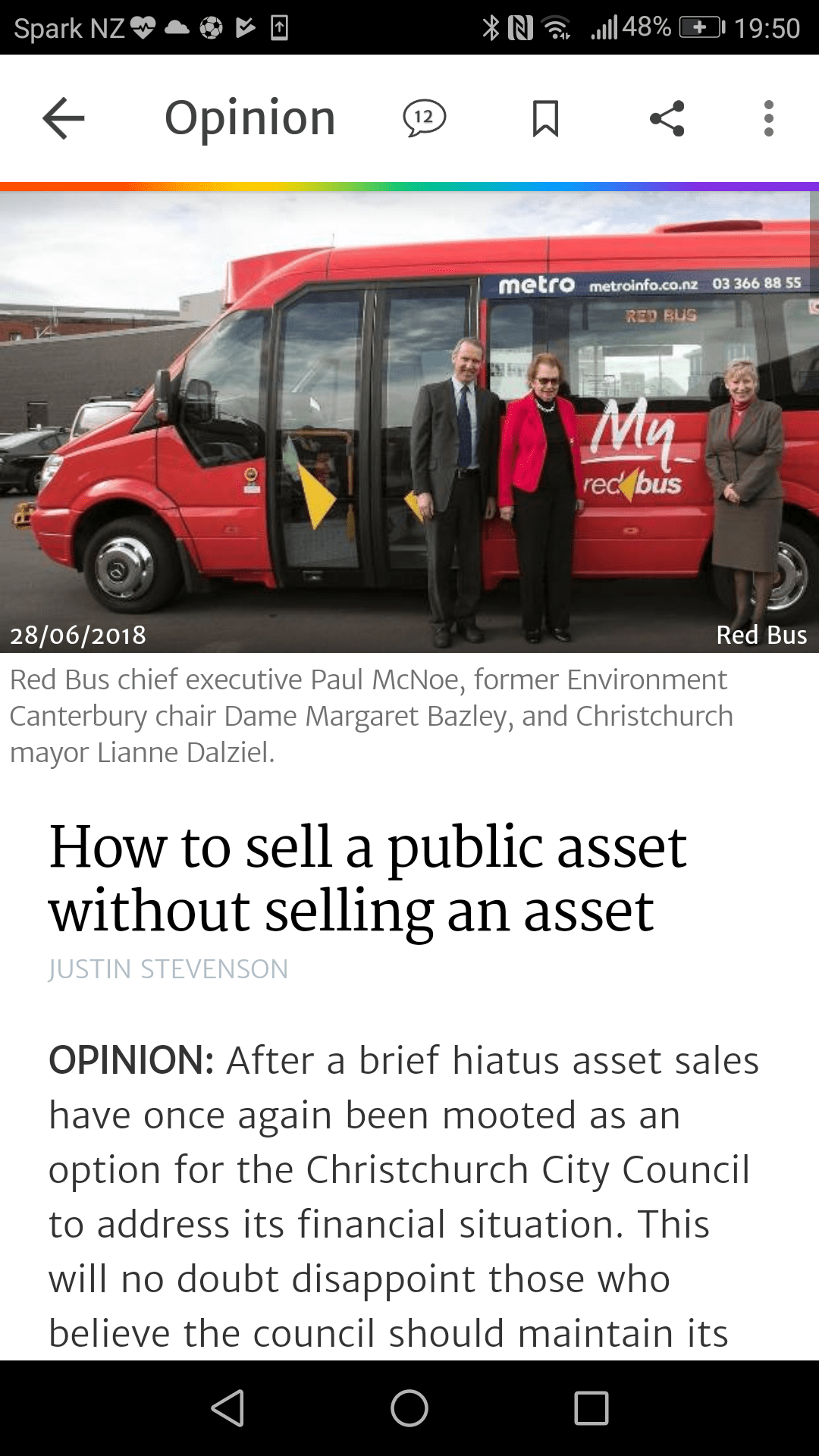

How to sell a public asset without selling an asset

After a brief hiatus asset sales have once again been mooted as an option for the Christchurch City Council to address its financial situation. This will no doubt disappoint those who believe the council should maintain its ownership stakes.

Those same people may be discouraged to learn that their opposition has not prevented a sell down on the sly. However, this is what appears to have happened with council owned Red Bus.

Red Bus is a bit of a problem child for the council and has been for many years. Not only does it struggle to retain bus routes in the face of private companies like Go Bus (an indicator of operational inefficiency for a public owned company), it barely makes a profit while sitting on a large amount of assets.

These assets could easily redeployed into better things (think “asset allocation” instead of asset sales), significantly benefiting the community.

While a good case could be made for selling Red Bus outright, it seems the risk of a PR backlash has meant that other avenues have been explored.

For example, the 2017 accounts indicated some odd behaviour. Despite make an operating profit of only $132,000 Red Bus was able to pay out a relatively hefty dividend of $1.35 million.

This is a good trick, but how was it achieved?

Despite a relatively small operating profit, a “consolidated profit” of $2.37 million was declared. For those wondering about the difference, the latter was largely the result of having extensive property assets revalued upwards by $2.38 million (+16%). A nice lift, but sitting on land and waiting for an increase in value is hardly a sign of managerial brilliance for a bus company. Pretty much all long term homeowners in New Zealand achieved this!

Red Bus then went to the bank, used the higher valuation to obtain a loan, and paid this money as a dividend to the CCC.

An equivalent situation would be using the increased value of your house to obtain a loan to pay for food. While it may be necessary at times, no one would suggest it makes you wealthier. You certainly cannot do it forever as eventually your equity runs out.

This is essentially what happened at Red Bus. The increase in value was sold to the bank for cash which was then passed onto the council.

This is called “releasing capital” which sounds better than “asset sales”, but both have the same effect of reducing the equity owned by the council.

Since paying a dividend of this size puts even more strain on a poorly performing company, significant pressure must have been applied. The substance of such actions are at odds to Mayor Lianne Dalziel’s statement that the council is “not considering asset sales”.

As it happens, selling down Red Bus is probably not a bad idea. Even in the latest financial year its return on assets was a miserable 0.8%. You could instead sell all the fixed assets in Red Bus, invest in a commercial property and receive 8 times as much for far less effort. Not doing so effectively costs rate payers around $2.3 million a year in lost income for no discernable benefit.

Although small compared to the overall council budget, $2.3 million a year is not chump change. There are clearly many good uses for this in Christchurch (I can certainly think of a few, can you?) and it is odd that the council has not taken advantage of this easy income stream.

The good news is that Red Bus is a small component of the council’s asset portfolio. With a bit more digging and some sensible asset allocation decisions the council’s financial position could be better than it appears.

_________________

Justin Stevenson has a Ph.D. in Engineering and a post-grad diploma in Economics. He really wants to see the city using its resources in a way that benefits the community the most.